ADVANCED DIPLOMA IN MANAGEMENT

ECONOMICS

ADVANCED DIPLOMA IN

MANAGEMENT

ECONOMICS

MODULE GUIDE

Copyright © 2021

REGENT BUSINESS SCHOOL

All rights reserved; no part of this book may be reproduced in any form or by any means, including

photocopying machines, without the written permission of the publisher.

ADVANCED DIPLOMA IN MANAGEMENT

1

ECONOMICS

Table of Contents

INTRODUCTION TO ECONOMICS ............................................................................... 3

CHAPTER 1:

Economic Systems ......................................................................................................... 8

CHAPTER 2:

Characteristics of Competitive Environments ............................................................... 98

CHAPTER 3:

Main Economic Policies ............................................................................................. 177

BIBLIOGRAPHY ........................................................................................................ 203

ADVANCED DIPLOMA IN MANAGEMENT

2

ECONOMICS

List of Tables and Figures

Figure 1.1: An example of a Production Possibilities Frontier (PPF) .............. 17

Figure 1.2.1: PPF & Marginal Costs highlighting allocative efficiencies ......... 19

Figure 1.2.2: PPF & Marginal Costs highlighting allocative efficiencies ......... 19

Figure 1.3: Economic Circular Flows .............................................................. 23

Figure 1.4: Demand Curve ............................................................................. 26

Figure 1.5: Price of related goods .................................................................. 27

Figure 1.6: Expected future prices ................................................................. 28

Figure 1.7: Increase in income ....................................................................... 29

Figure 1.8: Expected future income................................................................ 29

Figure 1.9: Population and demand .............................................................. 30

Figure 1.10: Preferences ................................................................................ 31

Figure 1.11: Change in the quantity demanded versus a change in demand. 32

Figure 1.12: Determining the price, quantity, income of factors of production 34

Figure 1.13: The effect of a shift of the demand curve ................................... 36

Figure 1.14: A change in quantity supplied versus a change in supply……… 37

Figure 1.15: Market equilibrium ...................................................................... 38

Figure 1.16: Changes in supply ...................................................................... 40

Figure 1.17: Categories of Price Elasticity of Demand ................................... 42

Figure 1.18: Total welfare - combined consumer & producer surplus ............ 52

Figure 1.19: Deadweight Loss from minimum wage....................................... 57

Figure 1.20: Effects of a tax on supply (sellers) ............................................. 59

Figure 1.21: Effects of a tax on demand (buyers) .......................................... 59

Figure 1.22: Perfectly price inelastic demand ................................................. 60

Figure 1.23: Perfectly price elastic demand) .................................................. 61

Figure 1.24: International Markets in Action ................................................... 65

Figure 1.25: Consumption Possibility Budget Line ......................................... 72

Figure 1.26: Paradox of value ........................................................................ 78

Figure 2.1: Product curve graph ..................................................................... 111

Figure 2.2.: Marginal Product Curve .............................................................. 112

Figure 2.3.: Average Product Curve ............................................................... 113

Figure 2.4.: The cost curve effect on production ............................................ 116

Figure 2.5.: Short-run supply curve ................................................................ 121

ADVANCED DIPLOMA IN MANAGEMENT

3

ECONOMICS

Figure 2.6.: The firm’s short-run shut-down decision...................................... 124

Figure 2.7.: Long-run supply curve ................................................................. 126

Figure 2.8.: Cost of Monopoly ........................................................................ 132

Figure 2.9.: Monopolistic competition in the short run .................................... 138

Figure 2.10.: Monopolistic competition in the long run ................................... 139

Figure 2.11: Oligopoly and Demand ............................................................... 141

Figure 2.12: Equilibrium Employment in a Competitive Labour Market .......... 145

Figure 2.13: Firm’s labour Demand Curve ..................................................... 148

Figure 2.14: An Individual’s Labour Supply Curve ......................................... 149

Figure 3.1: Laffer Curve .................................................................................. 184

Table 1.1: Maximising Utility ........................................................................... 74

Table 1.2: Marginal Utility per rand ................................................................ 76

Table 2.1: Marginal Revenue Product of Labour ............................................ 147

ADVANCED DIPLOMA IN MANAGEMENT

4

ECONOMICS

INTRODUCTION TO ECONOMICS

1. Introduction

Welcome to the Advanced Diploma in Management programme. As part of your

studies, you are required to study and successfully complete a course on

Economics.

2. Module Overview

Economics plays a role in our everyday life. By studying economics, it enables us to

understand past, future, and current economic models, and apply them to societies,

governments, businesses, and individuals. Economics uses scientific methods to

understand how scarce resources are exchanged within society. These can be

individual decisions, family decisions, business decisions or societal decisions.

Scarcity is a fact of life. Scarcity means that human wants for goods, services and

resources exceed what is available. Resources, such as labour, tools, land, and raw

materials are necessary to produce the goods and services we want but they exist in

limited supply. Of course, the ultimate scarce resource is time. Everyone, rich or

poor, has just twenty-four hours in the day to try to acquire the goods that they want.

At any point, there is only a finite number of resources available. Because these

resources are limited, so are the numbers of goods and services we produce with

them. Combine this with is the fact that human “wants” are virtually infinite. In this

module we will be discussing how market works, the impact of household choices

and the role of firms and markets in this. We will look at the different market failures

and governments response, factor markets, inequality and uncertainty, and the role

of governments in macro-policy development.

3. Aim of the Module

At the end of the module the student would be able to:

• Demonstrate an understanding of basic economic principles and concepts

ADVANCED DIPLOMA IN MANAGEMENT

5

ECONOMICS

• Distinguish between the various economic systems

• Elaborate on the concepts of supply and demand

• Illustrate the various forms of elasticity

• Discuss the types of unemployment and outline policies to combat

unemployment

• Discuss the concept of inflation and describe the tools that may be utilised

combat the effects of inflation

4. Essential (Prescribed) Reading

Your essential (prescribed) reading comprises the following:

4.1. Prescribed Reading

Parkin M, Kohler M, Lakay L, Rhodes B, Saayam A, Schoer V, Scholtz F,

Thompson K. (2019). Economics: Global and Southern African Perspectives.

3rd Edition. Pearson Education South Africa.

4.2. Recommended Reading

Harford, T (2007). The Undercover Economist. Random House. 3rd Edition.

USA.

5. How to use the Module

This module should be studied using the recommended and prescribed textbook/s in

conjunction with the relevant sections of this module. You must read about the topic

that you intend to study in the appropriate section before you start reading the

textbook/s in detail. Ensure that you make your own notes as you work through both

the textbook/s and this module. You will find a list of objectives and outcomes at the

beginning of each section. These outline the main points that you need to

understand when you have completed the section/s. The purpose of this guide is to

help you study. It is important for you to work through all the tasks and self-

assessment exercises as they provide guidelines for examination purposes.

ADVANCED DIPLOMA IN MANAGEMENT

6

ECONOMICS

6. Navigational Icons

Think Point

When you see this icon, you should think about and reflect on the

issues/challenges/themes presented.

Tasks

When you see this icon, you will know that you are required to

perform some kind of task to gauge how well you remember or

understand what you have read or how good you are at applying

what you have learnt.

Key Words and Definitions

This icon will alert you to a specific definition related to the topic

under discussion

Case Studies

Case studies are often used to illustrate a concept within the setting

of a real-life scenario. Answer the questions that follow to ensure

that you have a proper understanding of what has been discussed.

7. Specific Outcomes and Chapter Alignment

SPECIFIC PROGRAMME OUTCOMES

CHAPTER

ALIGNMENT

SO1:

Solve basic economic problems in different

economic systems.

Chapter 1

SO2:

Distinguish between the characteristics of the

various competitive environments.

Chapter 2

SO3:

Demonstrate an understanding of the main

economic policies.

Chapter 3

ADVANCED DIPLOMA IN MANAGEMENT

7

ECONOMICS

8. Specific Outcomes and Assessment Criteria

SPECIFIC PROGRAMME

OUTCOMES

ASSESSMENT CRITERIA

The student should demonstrate the

ability to:

SO1:

Solve basic economic

problems in different

economic systems.

• Apply and evaluate key terms,

concepts of supply and demand

whilst simultaneously considering

the impact of the forms of elasticity.

• Understand and be able to evaluate

knowledge scopes of competitive

environments and inflation.

• Identify, analyse, evaluate, critically

reflect on, and address complex

unemployment and related

problems, applying evidence-based

solutions and theory-driven

arguments when it comes to policy

development.

SO2:

Distinguish between the

characteristics of the various

competitive environments.

SO3:

Demonstrate an

understanding of the main

economic policies.

ADVANCED DIPLOMA IN MANAGEMENT

8

ECONOMICS

CHAPTER 1:

Economic Systems

Chapter Outcome

Upon completion of this chapter, the learner should be able to:

• Understand and evaluate knowledge of competitive environments and inflation.

1.1. Introduction to Economic Systems

An economic system is a means by which societies or governments organise and

distribute available resources, services, and goods across a geographic region or

country. Economic systems regulate the factors of production, including land, capital,

labour, and physical resources. An economic system encompasses many

institutions, agencies, entities, decision-making processes, and patterns of

consumption that comprise the economic structure of a given community. In this

chapter we will therefore be going over the concepts that determine economics, how

a market works and the different role players, and the choices that are available to

households.

Key Words and Definitions

Bear market: The principle of a bear market is simple enough.

Essentially, it represents a negative or pessimistic outlook on a stock

market’s performance, often with such markets falling into a downfall

spiral, where prices continue to drop. As a result of a bear market,

selling of stocks tends to increase. Additionally, investors expect, and

Think Point

What type of economic system do you think applies to your country?

ADVANCED DIPLOMA IN MANAGEMENT

9

ECONOMICS

may well receive, increased losses from their investments.

Bond: This is a debt-based investment that represents a promise to

pay from the bond issuer; the bond issuer owes money to bond

investors on a certain date

Bull market: A bull market represents a much more positive outlook

on a stock market’s performance compared to a bear market. In a

bull market, stock prices either have or are expected to increase.

Capital goods: These are items a business uses to produce goods

or services to sell to consumers; examples include manufacturing

equipment and business facilities.

Commodity: These are raw materials (like crude oil or iron ore) or

agricultural product (like unprocessed wheat or corn) purchased in

enormous quantities for production purposes.

Consumer: This is anyone (person or business) that uses

(consumes) goods or services.

Demand: The extent to which there is a market for goods or

services; when a lot of people want to buy something, demand is

high.

Elasticity: This is how much an economic variable changes in

response to another; if demand spikes when prices are low but

contract when prices are high, that is elastic demand.

Elasticity of demand: This describes how the demand for goods or

services increases or decreases when the price of that good or

service changes. Goods that generally are susceptible to the

elasticity of demand should exhibit the following patterns, namely, an

increase in the cost of the good will lead to a decrease in demand,

whereas a decrease in the cost of the good will lead to an increase in

demand.

ADVANCED DIPLOMA IN MANAGEMENT

10

ECONOMICS

Equity: This is the amount of ownership in an asset; the equity a

person has in their home is the difference between the property’s

value and the amount owed on the mortgage.

Financial markets This refers to a market or marketplace where

financial assets are bought and sold. A common example of a

financial market is a stock exchange.

Leverage: This is the extent to which an investment is funded with

borrowed money (debt); the investor is relying on earning a return in

order to pay off the debt and still make a profit.

Liquidity: This is the extent to which assets could quickly be

converted to cash; for example, a checking account is more liquid

than a one-year certificate of deposit.

Law of demand: The law of demand examines how customers’

buying habits change when prices increase. Specifically, the theory

posits that all other things being equal, when prices of a good

increase, the demand for that good will fall.

Law of supply: The law of supply states that all other things being

equal, an increase in price levels results in an increase in the quantity

of those goods that are supplied.

Market: This is any means that buyers and sellers use to exchange

money for goods or services.

Marginal utility: This refers to the amount of satisfaction a consumer

has by consuming a good or service. Marginal utility can be used by

economists to gauge how much of a good or service a consumer

should buy.

Opportunity cost: This is the cost of missing an opportunity in order

to take on a different opportunity. An example of opportunity cost can

be seen in investors, who may have to forego investing in one

ADVANCED DIPLOMA IN MANAGEMENT

11

ECONOMICS

company in order to invest in another.

Scarcity: These are resources or products that aren’t available in

unlimited quantities are scarce; as scarcity of an item increases, so

do prices.

Shift in demand: This is when the demand for a product or service

goes up or down due to factors other than a change in price.

Supply: This determines how much is available of a particular good

or service; when supply of a product goes down, the item becomes

scarce.

1.2. Introducing Economics

Economics is the social science that studies the choices that individuals, businesses,

governments, and entire societies make as they cope with scarcity and the

incentives that influence and reconcile those choices. It consists of two parts, namely

microeconomics and macroeconomics.

• Microeconomics: This is the study of the choices that individuals and

businesses make, the way these choices interact in markets and the influence of

governments. Some examples of microeconomic questions are: Why are people

downloading more movies and TV series? How would a tax on e-commerce

affect takealot.com?

• Macroeconomics: This is the study of the performance of the national economy

and the global economy. Some examples of macroeconomic questions are: Why

is the South African unemployment rate one of the highest in the world? Can the

South African Reserve Bank make our economy expand by cutting interest rates?

1.2.1. Understanding our changing world

Two big questions summarise the scope of economics:

ADVANCED DIPLOMA IN MANAGEMENT

12

ECONOMICS

• How do choices end up determining what, how and for whom goods and

services are produced?

• When do choices made in the pursuit of self-interest also promote the social

interest?

Goods and services: These are the objects that people value and produce to

satisfy human wants. Goods are physical objects such as cell phones and cars.

Services are tasks performed for people such as those at cell phone repair centres

and car service centres.

Production choices: What we produce varies across countries and changes over

time. The largest part (two-thirds, in fact) of what South Africa produces today is

services, such as retail and wholesale trade, health care and education. Goods are a

small part of total production.

Factors of production: This is described by the technologies and resources that we

use, and is grouped into four categories, namely land, labour, capital, and

entrepreneurship.

1. Land

In economics, land is what in everyday language we call natural resources. It

includes land in the everyday sense of the word together with minerals, oil, gas, coal,

water, air, forests, and fish. Our land surface and water resources are renewable and

some of our mineral resources can be recycled. But the resources that we use to

create energy, such as oil and coal, are non-renewable – they can be used only

once.

2. Labour

This is the work time and work effort that people devote to producing goods and

services. It includes the physical and mental efforts of all the people who work on

farms and construction sites and in factories, shops, and offices. The quality of

labour depends on human capital which is the knowledge and skills that people

obtain from education, on-the-job training, and work experience. One can build one’s

ADVANCED DIPLOMA IN MANAGEMENT

13

ECONOMICS

own human capital right now during the economics course, and one’s human capital

will continue to grow as work experience is gained.

3. Capital

These are the tools, instruments, machines, buildings, and other constructions that

businesses use to produce goods and services. Money, stocks, and bonds can also

be considered ‘capital’. These items are financial capital. Financial capital plays an

important role in enabling businesses to borrow the funds that they use to buy

capital. But financial capital is not used to produce goods and services, nor is it a

factor of production.

4. Entrepreneurship

This is the human resource that organises labour, land, and capital. They develop

new ideas about what and how to produce, make business decisions and bear the

risks that arise from these decisions.

The type of people that consume the different goods and services that are produced,

depends on the incomes that these different people earn. People with large incomes

can buy a wide range of goods and services. People with small incomes have fewer

options and can afford a smaller range of goods and services. People earn their

incomes by selling the services of the factors of production they own, such as:

• Land earns rent.

• Labour earns wages.

• Capital earns interest.

• Entrepreneurship earns profit.

Choices in the pursuit of self-interest and the promotion of social interest: All

the choices that people make about how to use their time and other resources are

made in the pursuit of self-interest, such as one’s time, budget and choices which

will influence how one feels about the choices made.

Social interest: An outcome is in the social interest if it is best for society as a

whole.

ADVANCED DIPLOMA IN MANAGEMENT

14

ECONOMICS

Efficiency and the social interest: Economists use the everyday word ‘efficient’ to

describe a situation that cannot be improved upon. Resource use is efficient if it is

not possible to make someone better off without making someone else worse off. If it

is possible to make someone better off without making anyone worse off, society can

be made better off, and the situation is not efficient.

Fair shares and the social interest: The idea that social interest requires "fair

shares" is deeply held. Fair shares do matter, but what is fair? People say that too

much inequality is unfair but how much is too much, and the inequality of what? Is it

income, or wealth, or the opportunity to work, to earn an income, and accumulate

wealth? There are four issues in today’s world that are related to these questions,

namely:

1. Globalisation

2. Information-age monopolies

3. Climate change

4. Economic instability

1. Globalisation

The term globalisation means the expansion of international trade, borrowing and

lending, and investment. While globalisation brings expanded production and job

opportunities for some workers, it destroys many domestic jobs. Workers across the

manufacturing industries must learn new skills, take service jobs, which often pay

less, or retire earlier than previously planned. Globalisation is in the self-interest of

those consumers who buy low-cost goods and services produced in other countries;

and it is in the self-interest of the multinational firms that produce in low-cost regions

and sell in high-price regions.

2. Information-age monopolies

The technological change of the past forty years has been called the Information

Revolution. The information revolution has clearly served one’s own self-interest; it

has provided tools such as smartphones, laptops, loads of handy applications, and

the internet. It has also served the self-interest of the owners of the companies that

supplied these goods.

ADVANCED DIPLOMA IN MANAGEMENT

15

ECONOMICS

3. Climate change

Every day, when a person makes self-interested choices to use electricity and petrol,

they contribute to their own carbon footprint, which can be lessened by walking,

riding a bike, taking a cold shower, or planting a tree – however, can each one of us

be relied upon to make decisions that affect the Earth’s carbon-dioxide concentration

in the social interest?

4. Economic instability

Banks’ choices to take deposits and make loans are made in self-interest, but does

this lending and borrowing serve the social interest? Do banks lend too much in the

pursuit of profit?

The questions that economics tries to answer tell us about the scope of economics,

but they do not tell us how economists think and go about seeking answers to these

questions, namely that:

1. A choice is a trade-off.

2. People make rational choices by comparing benefits and costs.

3. Benefit is what a person will gain from something.

4. Cost is what a person must give up in getting something.

5. Most choices are ‘how-much’ choices made at the margin.

6. Choices respond to incentives.

1. A choice is a trade-off

As we face scarcity, we must make choices. When we make a choice, we select

from the available alternatives. A trade-off is an exchange, to give up one thing, to

get something else.

2. People make rational choices by comparing benefits and costs

A rational choice is one that compares costs and benefits and achieves the greatest

benefit over cost for the person making the choice. Only the wants of the person

making a choice are relevant to determine its rationality.

ADVANCED DIPLOMA IN MANAGEMENT

16

ECONOMICS

3. Benefit is what a person will gain from something

The benefit of something is the gain or pleasure that it brings and is determined by

preferences, by what a person likes and dislikes and the intensity of those feelings.

Economists measure benefit as the most that a person is willing to give up getting

something.

4. Cost is what a person must give up in getting something

The opportunity cost of something is the highest-valued alternative that must be

given up getting it. It has two components: The things that a person cannot afford to

buy and the things that they cannot do with their time, such as the rand-value of that

time, or all the items that make up the opportunity cost. They involve choosing how

much of an activity to do.

5. Most choices are ‘how-much’ choices made at the margin

A person must decide how many minutes to allocate to each activity. The decision is

made at the margin. The benefit that arises from an increase in an activity is called

marginal benefit. The opportunity cost of an increase in an activity is called marginal

cost.

6. Choices respond to incentives.

The central idea of economics is that we can predict the self-interested choices that

people make by looking at the incentives they face. People undertake those activities

for which marginal benefit exceeds marginal cost; and they reject options for which

marginal cost exceeds marginal benefit. Economists see incentives as the key to

reconciling self-interest and social interest. When our choices are not in the social

interest, it is because of the incentives we face. One of the challenges for

economists is to figure out the incentives that result in self-interested choices being

in the social interest.

ADVANCED DIPLOMA IN MANAGEMENT

17

ECONOMICS

1.2.2. The Economic Problem

The quantities of goods and services that we can produce are limited both by our

available resources and by technology, if we want to increase our production of one

good, we must decrease the production of something else, we therefore face a

trade-off.

Figure 1.1. An example of a Production Possibilities Frontier (PPF)

Source: Creative Commons License

The production possibilities frontier (PPF): This is the boundary between those

combinations of goods and services that can be produced and those that cannot.

The PPF illustrates scarcity because we cannot attain the points outside the frontier.

These points describe wants that cannot be satisfied. We can produce at any point

inside the PPF or on the PPF, such as points A, B, C and D. F is attainable and is

inside the curve, but the products produced at this point would be wasted, or

misallocated, whereas E is outside the curve and not attainable

Production efficiency: We achieve production efficiency if we produce goods and

services at the lowest possible cost. This outcome occurs at all the points on the

PPF. Producing at any output level on the PPF implies the maximisation of

production given the available resources – hence the term production efficiency. At

points inside the PPF, production is inefficient because we are giving up more than

necessary of one good to produce a given quantity of the other good.

X

Y

ADVANCED DIPLOMA IN MANAGEMENT

18

ECONOMICS

Trade-off along the PPF: Every choice along the PPF involves a trade-off. Trade-

offs arise in every imaginable real-world situation in which a choice must be made.

At any given point in time, we have a fixed amount of labour, land, capital, and

entrepreneurship. By using our available technologies, we can employ these

resources to produce goods and services but are limited in what we can produce.

This limit defines a boundary between what we can attain and what we cannot attain.

This boundary is the real world’s production possibilities frontier, and it defines the

trade-offs that we must make. On our real-world PPF, we can produce more of any

one good or service only if we produce less of some other goods or services.

Opportunity cost: The opportunity cost of an action is the highest-valued alternative

forgone. The PPF makes this idea precise and enables us to calculate opportunity

cost. Along the PPF, there are only two goods, so there is only one alternative

forgone: some quantity of the other good.

• Opportunity cost is a ratio It is the decrease in the quantity produced of one

good divided by the increase in the quantity produced of another good as we

move along the production possibilities frontier.

Using resources efficiently: We achieve production efficiency at every point on the

PPF, but which point is best? The answer is the point on the PPF at which goods

and services are produced in the quantities that provide the greatest possible

benefit. When goods and services are produced at the lowest possible cost and in

the quantities that provide the greatest possible benefit, we have achieved allocative

efficiency.

The PPF and marginal cost: The marginal cost of a good is the opportunity cost of

producing one more unit of it. We calculate marginal cost from the slope of the PPF.

Preferences and marginal benefit: The marginal benefit from a good or service is

the benefit received from consuming one more unit of it. This benefit is subjective. It

depends on people’s preferences – people’s likes and dislikes and the intensity of

those feelings. Marginal benefit and preferences stand in sharp contrast to marginal

cost and production possibilities. Preferences describe what people like and want

and the production possibilities describe the limits or constraints on what is feasible.

We measure the marginal benefit from a good or service by the most that people are

ADVANCED DIPLOMA IN MANAGEMENT

19

ECONOMICS

willing to pay. Below one can see the allocative efficiencies that are demonstrated in

graph A versus the marginal costs in graph B.

Product X

Amount Product Y Amount Product Y

Graph A - PPF Graph B – Marginal cost

Figure 1.2.1. PPF & Marginal Costs highlighting allocative efficiencies

Source: Creative Commons License

To highlight this further, the PPF and opportunity cost (a) and the marginal cost

demonstrated in (b) are shown in cooldrinks, versus hamburgers, as such:

Figure 1.2.2. PPF & Marginal Costs highlighting allocative efficiencies

Source: Parkin M, et al. (2019). Economics: Global and Southern African

Perspectives. 3rd Edition. Pearson Education South Africa.

R

ADVANCED DIPLOMA IN MANAGEMENT

20

ECONOMICS

Allocative efficiency: At any point on the PPF, we cannot produce more of one

good without giving up some other good. At the best point on the PPF, we cannot

produce more of one good without giving up some other good that provides greater

benefit. We are producing at the point of allocative efficiency which is the point on

the PPF that we prefer above all other points.

Economic growth: The expansion of production possibilities is called economic

growth. Economic growth increases our standard of living, but it does not overcome

scarcity and avoid opportunity cost. To make our economy grow, we face a trade-off,

which means that the faster we make production grow, the greater is the opportunity

cost of economic growth.

The cost of economic growth: Economic growth comes from technological change

and capital accumulation. Technological change is the development of new goods

and of better ways of producing goods and services. Capital accumulation is the

growth of capital resources, including human capital. Technological change and

capital accumulation have vastly expanded our production possibilities.

A nation’s economic growth: If a nation devotes all its factors of production to

producing consumption goods and services and none to advancing technology and

accumulating capital, its production possibilities in the future will be the same as they

are today. To expand production possibilities in the future, a nation must devote

fewer resources to producing current consumption goods and services and some

resources to accumulating capital and developing new technologies. As production

possibilities expand, consumption in the future can increase. The decrease in today’s

consumption is the opportunity cost of tomorrow’s increase in consumption.

Gains from trade: People can produce for themselves all the goods and services

that they consume, or they can produce one good or a few goods and trade with

others. Producing only one good or a few goods is called specialisation. It is

therefore the ability of two agents to increase their consumption possibilities by

specialising in the good in which they have comparative advantage and trading for a

good in which they do not have comparative advantage

Comparative and absolute advantage: A person has a comparative advantage in

an activity if that person can perform the activity at a lower opportunity cost than

ADVANCED DIPLOMA IN MANAGEMENT

21

ECONOMICS

anyone else. Differences in opportunity costs arise from differences in individual

abilities and from differences in the characteristics of other resources.

• Absolute advantage describes a situation in which an individual, business or

country can produce more of a good or service than any other producer with

the same quantity of resources.

• Comparative advantage describes a situation in which an individual,

business or country can produce a good or service at a lower opportunity cost

than another producer.

• Production specialisation according to comparative advantage, not absolute

advantage, results in exchange opportunities that lead to consumption

opportunities beyond the PPC. Trade between two agents or countries allows

the countries to enjoy a higher total output and level of consumption than what

would have been possible domestically.

Achieving the gains from trade: Comparative advantage and opportunity costs

determine the terms of trade for exchange under which mutually beneficial trade can

occur. The terms of trade refer to the trading price agreed upon by two agents, which

when beneficial, will allow both countries to enjoy gains from trade.

Economic coordination: People gain by specialising in the production of those

goods and services in which they have a comparative advantage and then trading

with each other. For billions of individuals to specialise and produce millions of

different goods and services, their choices must somehow be coordinated. Two

competing economic coordination systems have been used namely, central

economic planning and decentralised markets.

• Central economic planning was tried in Russia and China and is still used in

Cuba and North Korea. This system works badly because government

economic planners do not know people’s production possibilities and

preferences. Resources get wasted, production ends up inside the PPF and

the wrong things get produced.

• Decentralised (market) coordination works best but to do so it needs four

complementary social institutions. They are:

1. Firms.

2. Markets.

ADVANCED DIPLOMA IN MANAGEMENT

22

ECONOMICS

3. Property rights.

4. Money.

1. Firms

A firm is an economic unit that hires factors of production and organises those

factors to produce and sell goods and services. Firms coordinate a huge amount of

economic

activity. Firms specialise in providing a particular product or service. The trade

between firms takes place in (decentralised) markets.

2. Markets

A market is any arrangement that enables buyers and sellers to get information and

to do business with each other. A market is therefore a network of producers, users,

wholesalers and brokers, or buyers that buy and sell products and services. These

networks deal with each other through telephone, computer, and other methods.

Markets facilitate trade. Enterprising individuals and firms, each pursuing their own

self-interest, have profited from making markets by standing ready to buy or sell the

items in which they specialise. Markets can only work however, when property rights

exist.

3. Property rights

The social arrangements that govern the ownership, use and disposal of anything

that people value is called property rights. Real property includes land and buildings,

those things we call property and durable goods such as plant and equipment.

Financial property includes stocks and bonds and money in the bank. Intellectual

property is the intangible product of creative effort. This type of property includes

books, music, computer programs and inventions of all kinds and is protected by

copyrights and patents. Where property rights are enforced, people have an

incentive to specialise and produce the goods in which they have a comparative

advantage. Where people can steal the production of others, resources are devoted

not to production but to protecting possessions.

ADVANCED DIPLOMA IN MANAGEMENT

23

ECONOMICS

4. Money

Money is any commodity or token that is generally acceptable as a means of

payment. Trade in markets can exchange any item for any other item. However, the

use of money makes trading in markets much more efficient.

Figure 1.3. Economic Circular Flows

Source: Creative Commons License

Circular flows through markets: There are the flows that result from the choices

that households and firms make. Households specialise and choose the quantities of

labour, land, capital, and entrepreneurial services to sell or rent to firms. Firms

choose the quantities of factors of production to hire. These flows go through to the

factor markets. Households choose the quantities of goods and services to buy, and

firms choose the quantities to produce. These flows then go through the goods

markets. Households receive incomes and make expenditures on goods and

services.

Coordinating decisions: Markets coordinate decisions through price adjustments.

Prices perform an economic function of major significance. So long as they are not

artificially controlled, prices provide an economic mechanism by which goods and

services are distributed among the large number of people desiring them. They also

act as indicators of the strength of demand for different products and enable

producers to respond accordingly. This system is known as the price mechanism

R

R

R

R

ADVANCED DIPLOMA IN MANAGEMENT

24

ECONOMICS

and is based on the principle that only by allowing prices to move freely will the

supply of any given commodity match demand. If supply is excessive, prices will be

low, and production will be reduced; this will cause prices to rise until there is a

balance of demand and supply. In the same way, if supply is inadequate, prices will

be high, leading to an increase in production that in turn will lead to a reduction in

prices until both supply and demand are in equilibrium.

1.3. How Markets Work

The market establishes the prices for goods and other services. These rates are

determined by supply and demand. Supply is created by the sellers, while demand is

generated by buyers. Markets try to find some balance in price when supply and

demand are themselves in balance.

1.3.1. Demand and Supply

A market has two sides: buyers and sellers. There are markets for goods, for, for

factors of production, and for other manufactured inputs. There are also markets for

money and for financial securities. Some markets are physical places where buyers

and sellers meet and where an auctioneer or a broker helps to determine the prices.

Some markets are groups of people spread around the world who never meet and

know little about each other but are connected through the internet or by tele-phone

and fax. Markets vary in the intensity of competition that buyers and sellers face.

Markets and prices: A competitive market is therefore a market that has many

buyers and many sellers, so no single buyer or seller can influence the price.

Producers offer items for sale only if the price is high enough to cover their

opportunity cost. And consumers respond to changing opportunity cost by seeking

cheaper alternatives to expensive items. In everyday life, the price of an object is the

amount of money that must be given up in exchange for it. Economists refer to this

price as the monetary value. The opportunity cost of an action is the highest-valued

alternative forgone. The ratio of one price to another is called a relative price and a

relative price is an opportunity cost. The normal way of expressing a relative price is

in terms of a ‘basket’ of all goods and services. To calculate this relative price, we

ADVANCED DIPLOMA IN MANAGEMENT

25

ECONOMICS

divide the money price of a good by the money price of a ‘basket’ of all goods (called

a price index). The resulting relative price tells us the opportunity cost of the good in

terms of how much of the ‘basket’ we must give up buying it. The demand and

supply model that we are about to study determines relative prices and the word

‘price’ means relative price. When we predict that a price will fall, we do not mean

that its money price will fall, it is that its relative price will fall. Its price will fall relative

to the average price of other goods and services.

Demand: If a person demands something, then they want it, can afford it and plan to

buy it. Wants are the unlimited desires or wishes that people have for goods and

services. Demand reflects a decision about which wants to satisfy. The quantity

demanded of a good or service is the amount that consumers plan to buy during a

given time period at a particular price. The quantity demanded is not necessarily the

same as the quantity actually bought. Sometimes the quantity demanded exceeds

the amount of goods available, so the quantity bought is less than the quantity

demanded. The quantity demanded is measured as an amount per unit of time.

Law of demand: This law states that where other things remaining the same, the

higher the price of a good, the smaller is the quantity demanded; and the lower the

price of a good, the greater is the quantity demanded. A higher price will reduce the

quantity demanded due to:

1. Substitution effect.

2. Income effect.

1. Substitution effect

When the price of a good rises, other things remaining the same, its relative price, its

opportunity cost rises. Although each good is unique, it has substitutes – other goods

that can be used in its place. As the opportunity cost of a good rises, people buy less

of that good and more of its substitutes.

2. Income effect

When a price rises and all other influences on buying plans remain unchanged, the

price rises relative to people’s incomes. So faced with a higher price and an

ADVANCED DIPLOMA IN MANAGEMENT

26

ECONOMICS

unchanged income, people cannot afford to buy all the things they previously bought.

They must decrease the quantities demanded of at least some goods and services

and normally, the good whose price has increased will be one of the goods that

people buy less of.

Figure 1.4. Demand Curve

Source: Creative Commons License

Demand curve and demand schedule: The term demand refers to the entire

relationship between the price of the good and the quantity. demanded of the good.

Demand is illustrated by the demand curve and the demand schedule. The term

quantity demanded refers to a point on a demand curve which is the quantity

demanded at a particular price.

• A demand curve shows the relationship between the quantity demanded of a

good and its price when all other influences on consumers’ planned

purchases remain the same.

• A demand schedule lists the quantities demanded at each price when all the

other influences on consumers’ planned purchases remain the same.

Another way of looking at the demand curve is as a willingness-and-ability-to-pay

curve. The willingness and ability to pay is a measure of marginal benefit. If a small

quantity is available, the highest price that someone is willing and able to pay for one

more unit is high. But as the quantity available increases, the marginal benefit of

each additional unit falls and the highest price that someone is willing and able to

pay also falls along the demand curve.

ADVANCED DIPLOMA IN MANAGEMENT

27

ECONOMICS

A change in demand: When any factor that influences buying plans changes, other

than the price of the good, there is a change in demand. Six main factors bring

changes in demand. They are changes in:

1. The prices of related goods.

2. Expected future prices.

3. Income.

4. Expected future income and credit.

5. Population.

6. Preferences.

1. The prices of related goods

The quantity of a product that consumers plan to buy depends in part on the prices

of substitutes for that product. A substitute is a good that can be used in place of

another good. A complement is a good that is used in conjunction with another good.

Figure 1.5. Price of related goods

Source: Creative Commons License

ADVANCED DIPLOMA IN MANAGEMENT

28

ECONOMICS

2. Expected future prices

If the expected future price of a good rises and if the good can be stored, the

opportunity cost of obtaining the good for future use is lower today than it will be in

the future when people expect the price to be higher. So people retime their

purchases which they substitute over time. They buy more of the good now before its

price is expected to rise (and less afterward), so the demand for the good today

increases. Similarly, if the expected future price of a good falls, the opportunity cost

of buying the good today is high relative to what it is expected to be in the future. So

again, people retime their purchases. They buy less of the good now before its price

is expected to fall, so the demand for the good decreases today and increases in the

future. This can be demonstrated by the example below where a change in the price

of oil, will cause the quantity of oil supplied to change.

Figure 1.6. Expected future prices

Source: Creative Commons License

3. Income

Consumers’ income influences demand. When income increases, consumers buy

more of most goods; and when income decreases, consumers buy less of most

goods. Although an increase in income leads to an increase in the demand for most

goods, it does not lead to an increase in the demand for all goods. A normal good is

ADVANCED DIPLOMA IN MANAGEMENT

29

ECONOMICS

one for which demand increases as income increases. An inferior good is one for

which demand decreases as income increases.

Figure 1.7. Increase in income

Source: Creative Commons License

4. Expected future income and credit

When expected future income increases or credit becomes easier to get, demand for

the good might increase now, as can be seen in panel (a), versus a decrease in

income in panel (b).

Figure 1.8. Expected future income

Source: Creative Commons License

ADVANCED DIPLOMA IN MANAGEMENT

30

ECONOMICS

5. Population

Demand also depends on the size and the age structure of the population. The

larger the population, the greater the demand for all goods and services is; the

smaller the population, the smaller the demand for all goods and services is. Also,

the larger the proportion of the population in a given age group, the greater the

demand for the goods and services used by that age group is, such as this diagram

for the expected demand in education from 1970 to 2100, this is per region, globally.

Figure 1.9. Population and demand

Source: Creative Commons License

6. Preferences

Preferences determine the value that people place on each good and service.

Preferences depend on such things as the weather, information, and fashion. The

diagram below demonstrates that consumer’s preference for a particular product are

inconsistent.

ADVANCED DIPLOMA IN MANAGEMENT

31

ECONOMICS

Figure 1.10. Preferences

Source: Creative Commons License

A change in the quantity demanded versus a change in demand: Changes in

the influences on buying plans bring either a change in the quantity demanded or a

change in demand. Equivalently, they bring either a movement along the demand

curve or a shift of the demand curve. The distinction between a change in the

quantity demanded and a change in demand is the same as that between a

movement along the demand curve and a shift of the demand curve. A point on the

demand curve shows the quantity demanded at a given price, so a movement along

the demand curve shows a change in the quantity demanded. The entire demand

curve shows demand, so a shift of the demand curve shows a change in demand.

• Movement along the demand curve: If the price of the good changes but no

other influence on buying plans changes, we illustrate the effect as a

movement along the demand curve. This can be seen in Graph A, where

there is a movement along the curve, there is a change in the price of a

product and the other factors remain constant.

• A shift of the demand curve: If the price of a good remains constant but

some other influence on buying plans changes, there is a change in demand

ADVANCED DIPLOMA IN MANAGEMENT

32

ECONOMICS

for that good. We illustrate a change in demand as a shift of the demand

curve. This can be seen in Graph B.

Graph A Graph B

Figure 1.11. Change in the quantity demanded versus a change in demand

Source: Creative Commons License

Supply: If a firm supplies a good or service, the firm has the resources and

technology to produce it, can profit from producing it and plans to produce it and sell

it. The quantity supplied of a good or service is the amount that producers plan to

sell during a given time period at a particular price. The quantity supplied is not

necessarily the same amount as the quantity actually sold. Sometimes the quantity

supplied is greater than the quantity demanded, so the quantity sold is less than the

quantity supplied. Like the quantity demanded, the quantity supplied is measured as

an amount per unit of time.

The law of supply: When other things remaining the same, the higher the price of a

good, the greater the quantity supplied; and the lower the price of a good, the

smaller the quantity supplied. A higher price increases the quantity supplied because

marginal cost increases. As the quantity produced of any good increases, the

marginal cost of producing the good increases. When the price of a good rises, other

things remaining the same, producers are willing to incur a higher marginal cost, so

they increase production. The higher price leads to an increase in the quantity

supplied.

ADVANCED DIPLOMA IN MANAGEMENT

33

ECONOMICS

Supply curve and supply schedule: The term supply refers to the entire

relationship between the price of a good and the quantity supplied of it. Supply is

illustrated by the supply curve and the supply schedule. The term quantity supplied

refers to a point on a supply curve – the quantity supplied at a particular price. A

supply curve shows the relationship between the quantity supplied of a good and its

price when all other influences on producers’ planned sales remain the same. The

supply curve is a graph of a supply schedule. The supply curve can be interpreted as

a minimum-supply-price curve – a curve that shows the lowest price at which

someone is willing to sell. This lowest price is the marginal cost. If a small quantity is

produced, the lowest price at which someone is willing to sell one more unit is low.

But as the quantity produced increases, the marginal cost of each additional unit

rises, so the lowest price at which someone is willing to sell an additional unit rises

along the supply curve.

A change in supply: When any factor that influences selling plans other than the

price of the good changes, there is a change in supply. Six main factors bring

changes in supply. They are changes in:

1. the prices of factors of production

2. the prices of related goods produced

3. expected future prices

4. the number of suppliers

5. technology

6. the state of nature

1. The prices of factors of production

The prices of the factors of production used to produce a good influence its supply.

To see this influence, think about the supply curve as a minimum-supply-price curve.

If the price of a factor of production rises, the lowest price that a producer is willing to

accept for that good rise, so supply decreases.

The market price of any commodity is determined by the impersonal forces of

demand and supply. In the figure on the next page, the demand and supply curves

for some factors of production are D1 and S. The equilibrium price and quantity are

p1 and q1, respectively. The total income earned by the factor is indicated by the

ADVANCED DIPLOMA IN MANAGEMENT

34

ECONOMICS

area Op1 Eq1 (which is Op1 x Oq1). This assumes that the price of all other factors

of production, the prices of all goods, and the level of national income are given

constants. Fluctuations in the equilibrium price and quantity may cause fluctuation in

the return to the factor, in its relative earnings (compared to other factors) and in the

share of national income going to the factor. Suppose the demand curve for the

factor in question shifts from D1 to D2. Now the price of the factor rises from p1 to p2

and the quantity of the factor demanded (employed) rises from q1 to q2 So the total

earnings rise from p1q1 to p2q2 and if the total income in the whole economy

remains constant at a then the share of income going to this factor rises from p1q1/α

to p2q2/α. This is the essence of the free-market determination of a factor’s price

and its share of national income.

Figure: 1.12. Determining the price, quantity, income of factors of production

Source: Creative Commons License

2. The prices of related goods produced

The price of related goods is one of the other factors affecting demand. Related

goods are classified as either substitutes or complements. Substitutes are goods that

satisfy a similar need or desire. An increase in the price of a good will increase

demand for its substitute, while a decrease in the price of a good will decrease

demand for its substitute. Complements are goods that are used jointly. An increase

in the price of a good will decrease demand for its complement while a decrease in

the price of a good will increase demand for its complement.

ADVANCED DIPLOMA IN MANAGEMENT

35

ECONOMICS

3. Expected future prices

If the expected future price of a good rises, the return from selling the good in the

future increases and is higher than it is today. So, supply decreases today and

increases in the future.

4. The number of suppliers

The larger the number of firms that produce a good, the greater is the supply of the

good. As new firms enter an industry, the supply in that industry increases. As firms

leave an industry, the supply in that industry decreases.

5. Technology

The term ‘technology’ is used broadly to mean the way that factors of production are

used to produce a good. A technology change occurs when a new method is

discovered that lowers the cost of producing a good.

6. The state of nature

The state of nature includes all the natural forces that influence production. It

includes the state of the weather and, more broadly, the natural environment. Good

weather can increase the supply of many agricultural products and bad weather can

decrease their supply. Extreme natural events such as earthquakes, hurricanes and

severe droughts can also influence supply.

ADVANCED DIPLOMA IN MANAGEMENT

36

ECONOMICS

Figure 1.13. The effect of a shift of the demand curve

Source: Creative Commons License

A change in the quantity supplied versus a change in supply: Either a change in

the quantity supplied or a change in supply. Equivalently, they bring either a

movement along the supply curve or a shift of the supply curve. A point on the

supply curve shows the quantity supplied at a given price. A movement along the

supply curve shows a change in the quantity supplied. The entire supply curve

shows supply. A shift of the supply curve shows a change in supply which is

demonstrated below. A change in supply leads to a shift in the supply curve, which

causes an imbalance in the market that is corrected by changing prices and demand.

An increase in the change in supply shifts the supply curve to the right, while a

decrease in the change in supply shifts the supply curve left. Essentially, there is an

increase or decrease in the quantity supplied that is paired with a higher or lower

supply price. A change in supply shouldn't be confused with a change in the quantity

supplied. The former causes a shift in the entire supply curve, while the latter results

in movement along the existing supply curve.

ADVANCED DIPLOMA IN MANAGEMENT

37

ECONOMICS

Figure 1.14. A change in quantity supplied versus a change in supply

Source: Creative Commons License

Market equilibrium: An equilibrium is a situation in which opposing forces balance

each other. Equilibrium in a market occurs when the price balances buying plans and

selling plans. The equilibrium price is the price at which the quantity demanded

equals the quantity supplied. The equilibrium quantity is the quantity bought and sold

at the equilibrium price. A market moves toward its equilibrium because price

regulates buying and selling plans, or price adjusts when plans do not match.

• Price as regulator: The price of a good regulates the quantities demanded

and supplied. If the price is too high, the quantity supplied exceeds the

quantity demanded. If the price is too low, the quantity demanded exceeds the

quantity supplied. There is one price at which the quantity demanded equals

the quantity supplied.

• Price adjustments: If the price is below equilibrium, there is a shortage and

that if the price is above equilibrium, there is a surplus. the price can also

change and eliminate a shortage or a surplus.

o A shortage forces the price up: Some producers, noticing lines of

unsatisfied consumers, raise the price. Some producers increase their

output. As producers push the price up, the price rises toward its

equilibrium. The rising price reduces the shortage because it

decreases the quantity demanded and increases the quantity supplied.

When the price has increased to the point at which there is no longer a

shortage, the forces moving the price stop operating and the price

comes to rest at its equilibrium.

ADVANCED DIPLOMA IN MANAGEMENT

38

ECONOMICS

o A surplus forces the price down: As producers cut the price, the

price falls toward its equilibrium. The falling price decreases the surplus

because it increases the quantity demanded and decreases the

quantity supplied. When the price has fallen to the point at which there

is no longer a surplus, the forces moving the price stop operating and

the price comes to rest at its equilibrium.

o The best deal available for buyers and sellers: When the price is

above equilibrium, it is bid down-ward. Why do sellers not resist this

decrease and refuse to sell at the lower price? The answer is because

their minimum supply price is below the current price, and they cannot

sell all they would like to at the current price. Sellers willingly lower the

price to gain market share. At the price at which the quantity demanded

and the quantity supplied are equal, neither buyers nor sellers can do

business at a better price. Buyers pay the highest price they are willing

to pay for the last unit bought and sellers receive the lowest price at

which they are willing to supply the last unit sold.

Figure 1.15. Market Equilibrium

Source: Creative Commons License

Because the graphs for demand and supply curves both have price on the vertical

axis and quantity on the horizontal axis, the demand curve and supply curve for a

particular good or service can appear on the same graph. Together, demand and

price

per

gallon

X

Y

ADVANCED DIPLOMA IN MANAGEMENT

39

ECONOMICS

supply determine the price and the quantity that will be bought and sold in a market.

The demand curve, D and the supply curve, S, intersect at the equilibrium point E,

with an equilibrium price of 1.4 and an equilibrium quantity of 600. The equilibrium is

the only price where quantity demanded is equal to quantity supplied. At a price

above equilibrium, like 1.8, quantity supplied exceeds the quantity demanded, so

there is excess supply. At a price below equilibrium, such as 1.2, quantity demanded

exceeds quantity supplied, so there is excess demand.

Predicting changes in price and quantity: The demand and supply model that we

have just studied provides us with a powerful way of analysing influences on prices

and the quantities bought and sold. According to the model, a change in price stems

from a change in demand, a change in supply, or a change in both demand and

supply.

An increase in demand: When more people receive higher incomes, the demand

for products increase. The increase in demand creates a shortage at the original

price and to eliminate the shortage, the price must rise.

A decrease in demand: We can reverse this change in demand if demand

decreases to its original level. Such a decrease in demand might arise if people

switch to substitute for the product. The decrease in demand shifts the demand

curve leftward.

An increase in supply: When supply increases, the supply curve shifts rightward.

there is an increase in the quantity demanded but no change in demand, a

movement along, but no shift of, the demand curve. When supply increases, the

price falls and the quantity increases.

A decrease in supply: The decrease in supply shifts the supply curve leftward.

When supply decreases, the price rises and the quantity decreases.

All the possible changes in demand and supply: The effects of a change in either

demand or supply means that one can predict what happens if both demand and

supply change together.

• Change in demand with no change in supply: With an increase in supply

and no change in demand, the price falls and quantity increases. With a

ADVANCED DIPLOMA IN MANAGEMENT

40

ECONOMICS

decrease in supply and no change in demand, the price rises and the quantity

decreases.

• Increase in both demand and supply: Because either an increase in

demand or an increase in supply increases the quantity, the quantity also

increases when both demand and supply increase. But the effect on the price

is uncertain. An increase in demand raises the price and an increase in supply

lowers the price, so we cannot say whether the price will rise or fall when the

magnitudes of the changes in demand and supply to predict the effects on

price.

• Decrease in both demand and supply: When both demand and supply

decrease, the quantity decreases, and again the direction of the price change

is uncertain.

• Decrease in demand and increase in supply: Both the decrease in demand

and the increase in supply lower the price, so the price falls. But a decrease in

demand decreases the quantity and an increase in supply increases the

quantity, so we cannot predict the direction in which the quantity will change

unless we know the magnitudes of the changes in demand and supply.

• Increase in demand and decrease in supply: The price will rise and again

the direction of the quantity change is uncertain.

1.3.2. Elasticity

Elasticity is an economic measure of how sensitive an economic factor is to another,

for example, changes in supply or demand to the change in price, or changes in

demand to changes in income.

Figure 1.16. Changes in Supply

Source: Creative Commons License

ADVANCED DIPLOMA IN MANAGEMENT

41

ECONOMICS

Price elasticity of demand: This is a measurement of the change in consumption of

a product in relation to a change in its price. When supply increases, the equilibrium

price falls, and the equilibrium quantity increases. Price elasticity of demand is a

measurement of the change in consumption of a product in relation to a change in its

price. A good is elastic if a price change causes a substantial change in demand or

supply. A good is inelastic if a price change does not cause demand or supply to

change very much. The availability of a substitute for a product affects its elasticity. If

there are no good substitutes and the product is necessary, demand won’t change

when the price goes up, making it inelastic. The price elasticity of demand is a units-

free measure of the responsiveness of the quantity demanded of a good to a change

in its price when all other influences on buying plans remain the same.

Calculating price elasticity of demand: Expressed mathematically, it is:

Price Elasticity of Demand = Percentage Change in Quantity Demanded /

Percentage Change in Price

Notice that we use the average price and average quantity. We do this because it

gives the most precise measurement of elasticity, at the midpoint between the

original price and the new price. Elasticity is the ratio of two percentage changes, so

when we divide one percentage change by another, the 100s cancel. A percentage

change is a proportionate change multiplied by 100. Elasticity is a units-free measure

because the percentage change in each variable is independent of the units in which

the variable is measured. The ratio of the two percentages is a number without units.

When the price of a good rises, the quantity demanded decreases. Because a

positive change in price brings a negative change in the quantity demanded, the

price elasticity of demand is a negative number. But it is the magnitude, or absolute

value, of the price elasticity of demand that tells us how responsive the quantity

demanded is.

ADVANCED DIPLOMA IN MANAGEMENT

42

ECONOMICS

Figure 1.17. Categories of Price Elasticity of Demand

Source: Creative Commons License

Inelastic and elastic demand: There are three demand curves that cover the entire

range of possible elasticities of demand. If the quantity demanded remains constant

when the price changes, then the price elasticity of demand is zero and the good is

said to have a perfectly inelastic demand. If the percentage change in the quantity

demanded equals the percentage change in the price, then the price elasticity equals

1 and the good is said to have a unit elastic demand. The general case in which the

percentage change in the quantity demanded is less than the percentage change in

the price. In this case, the price elasticity of demand is between zero and 1 and the

good is said to have an inelastic demand. If the quantity demanded changes by an

infinitely large percentage in response to a tiny price change, then the price elasticity

of demand is infinity and the good is said to have a perfectly elastic demand. If the

price elasticity of demand is greater than 1 and the good is said to have an elastic

demand. When demand is perfectly inelastic, quantity demanded for a good does not

change in response to a change in price. Finally, demand is said to be perfectly

elastic when the PED coefficient is equal to infinity. When demand is perfectly

elastic, buyers will only buy at one price and no other.

Elasticity along a linear demand curve: Elasticity and slope are not the same. A

linear demand curve has a constant slope, but a varying elasticity and the price

elasticity of demand varies depending on the interval over which we are measuring

it. For any linear demand curve, the absolute value of the price elasticity of demand

ADVANCED DIPLOMA IN MANAGEMENT

43

ECONOMICS

will fall as we move down and to the right along the curve. The lower the price and

the greater the quantity demanded, the lower the absolute value of the price

elasticity of demand.

Total revenue and elasticity: The total revenue from the sale of a good equals the

price of the good multiplied by the quantity sold. When a price changes, total

revenue also changes. But a cut in the price does not always decrease total

revenue. The change in total revenue depends on the elasticity of demand in the

following way:

• If demand is elastic: A 1 % price cut increases the quantity sold by more

than 1 % and total revenue increases.

• If demand is inelastic: A 1 % price cut increases the quantity sold by less

than 1 % and total revenue decreases.

• If demand is unit elastic: A 1 % price cut increases the quantity sold by 1 %

and total revenue does not change.

Expenditure and elasticity: When prices change, the change in one’s expenditure

on the good depends on the elasticity of demand.

• If demand is elastic: A 1 % price cut increases the quantity bought by more

than 1 % and expenditure on the item increases.

• If demand is inelastic: A 1 % price cut increases the quantity bought by less

than 1 % and expenditure on the item decreases.

• If demand is unit elastic: A 1 % price cut increases the quantity bought by 1

% and the expenditure on the item does not change.

So, if one spends more on an item when its price falls, the demand for that item is

elastic; if one spends the same amount, the demand is unit elastic; and if one

spends less, the demand is inelastic

The factors that influence the elasticity of demand: The elasticity of demand for a

good depends on:

1. The closeness of substitutes.

2. The proportion of income spent on the good.

3. The time elapsed since the price change.

ADVANCED DIPLOMA IN MANAGEMENT

44

ECONOMICS

1. The closeness of substitutes

The closer the substitutes for a good or service, the more elastic is the demand for it.

The degree of substitutability depends on how narrowly (or broadly) we define a

good. In everyday language we call goods such as food and shelter necessities and

goods such as exotic holidays luxuries. A necessity has poor substitutes and is

crucial for our well-being. So, a necessity generally has an inelastic demand. A

luxury usually has many substitutes, one of which is not buying it. So, a luxury

generally has an elastic demand.

2. The proportion of income spent on the good

Other things remaining the same, the greater the proportion of income spent on a

good, the more elastic (or less inelastic) is the demand for it.

3. The time elapsed since the price change.

The longer the time that has elapsed since a price change, the more elastic is

demand.

Cross elasticity of demand: We measure the influence of a change in the price of a

substitute or complement by using the concept of the cross elasticity of demand. The

cross elasticity of demand is a measure of the responsiveness of the demand for a

good to a change in the price of a substitute or complement, other things remaining

the same. We calculate the cross elasticity of demand by using the formula:

Percentage change in quantity demanded

Cross elasticity of demand = Percentage change in price of a substitute or

complement

The cross elasticity of demand can be positive or negative. It is positive for a

substitute and negative for a complement.

ADVANCED DIPLOMA IN MANAGEMENT

45

ECONOMICS

• Substitutes: Substitutes are goods where one can consume one in place of

the other. The price elasticity of demand for a good or service will be greater

in absolute value if many close substitutes are available for it. If there are lots

of substitutes for a particular good or service, then it is easy for consumers to

switch to those substitutes when there is a price increase for that good or

service. If a good has no close substitutes, its demand is likely to be

somewhat less price elastic.

• Complements: These are goods that are consumed together.

The prices of complementary or substitute goods also shift the demand curve. When

the price of a good that complements a good decrease, then the quantity demanded

of the one increase and the demand for the other increases. When the price of a

substitute good decreases, the quantity demanded for those goods increases, but

the demand for the good that it is being substituted for decreases. he magnitude of

the cross elasticity of demand determines how far the demand curve shifts. The

larger the cross elasticity (absolute value), the greater is the change in demand and

the larger is the shift in the demand curve. If two items are close substitutes, such as

two brands of spring water, the cross elasticity is large. If two items are close

complements, such as movies and popcorn, the cross elasticity is large. If two items

are somewhat unrelated to each other, such as university textbooks and haircuts, the

cross elasticity is small, perhaps even zero.

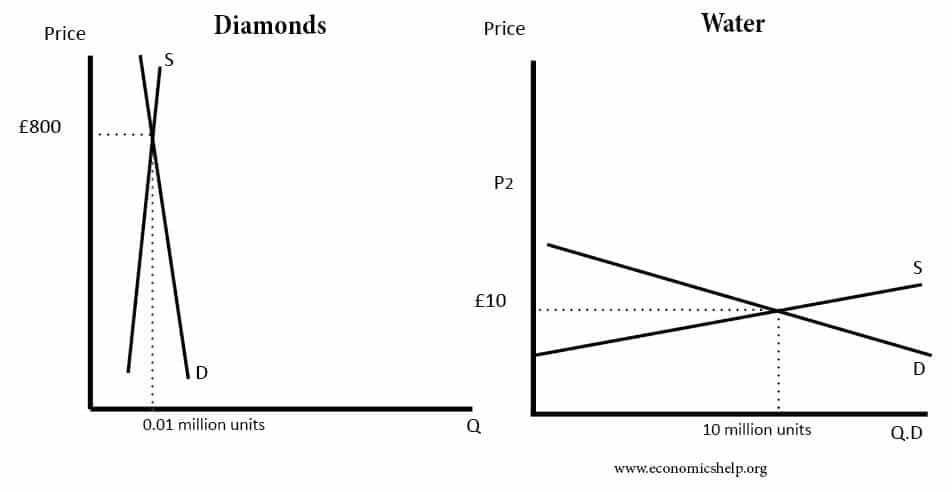

Income elasticity of demand: Suppose the economy is expanding and people are

enjoying rising incomes. This prosperity brings an increase in the demand for most

types of goods and services. It therefore depends on the income elasticity of

demand, which is a measure of the responsiveness of the demand for a good or

service to a change in income, other things remaining the same. he income elasticity

of demand is calculated by using the formula:

Percentage change in quantity demanded

Income elasticity of demand = Percentage change in income